InvestBot

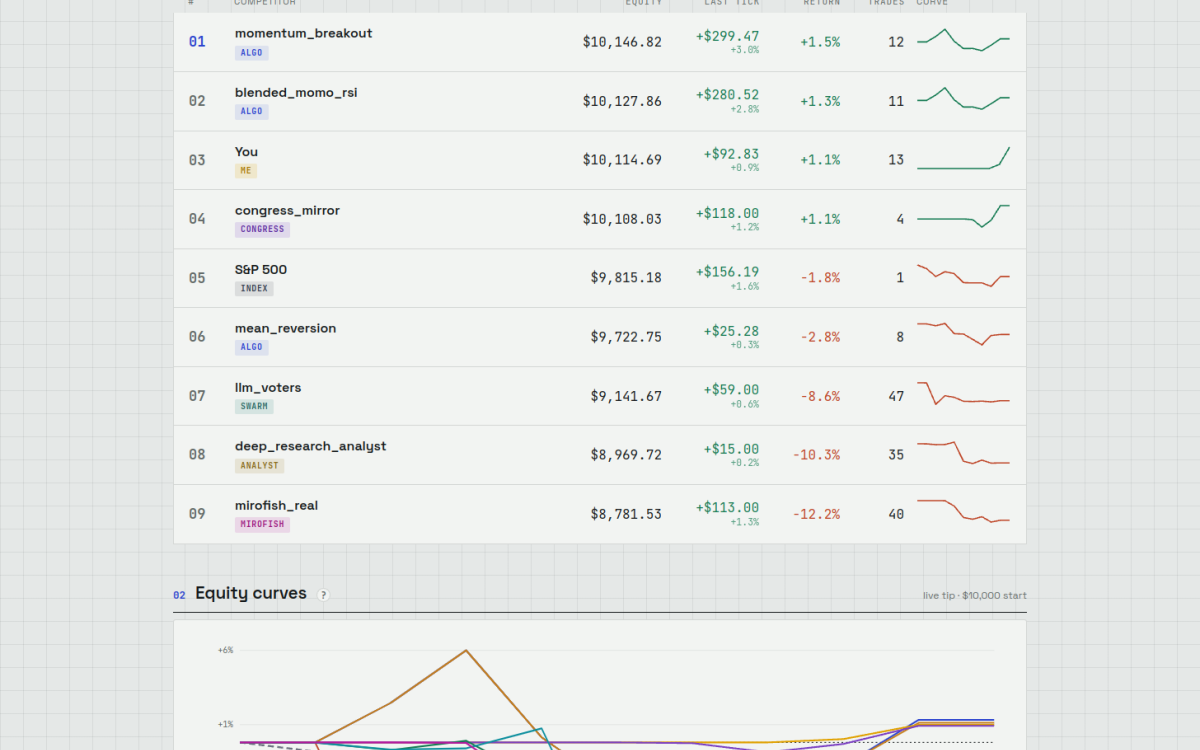

A local, paper-money trading bake-off — several approaches each manage their own virtual $100 over the same ~100-name market, so you get an apples-to-apples leaderboard of what actually works before risking a real dollar.

⚠️ Paper money only. The Robinhood broker is an intentional stub — nothing here places a real order. Going live is gated behind a graduation bar (survived a drawdown, enough decisions, tolerable max drawdown).

The competitors

Every competitor starts from the same stake and trades the same market; the dashboard ranks them with full click-through provenance and overlays the S&P 500 as a benchmark.

- Rule strategies — a 20-day momentum breakout, an RSI mean-reversion, and a blended momentum/RSI strategy that skips already-overbought entries.

- Research analyst — runs Anthropic's Claude for Financial Services equity-research methodology each tick (screen → sector → comps → catalysts → thesis → portfolio), then grades its prior call against the market and adjusts.

- LLM swarm (

llm_voters) — 150 cheap LLMs, each a uniquepersona × risk × horizon × quirk, voting on its own random slice of the market: an independent-voter election whose disjoint slices keep votes from herding. - Social swarm (

mirofish_real) — persona agents with memory that interact over rounds; the book follows their rank-weighted consensus. - Congress mirror — ranks members of Congress by the excess return of their disclosed STOCK Act trades, then buys what the top performers bought (on the disclosure date, which by law lags the real trade by up to ~45 days).

The dashboard

A Next.js app that fetches the bake-off state, live-polls real prices (Finnhub), pulls headlines, and lets you click any ticker for its price chart with each method's buy/sell markers. Equity curves overlay the S&P 500 as a dashed benchmark; the decision trail is colour-coded by method with per-method filtering.

Risk controls (the "not gambling" part)

A hard per-position stop-loss, a cap on open positions, an equity circuit breaker that halts new buys after a drawdown, and simulated slippage on every fill so paper results aren't flattering.

Tech Stack

- Engine: stdlib-only Python backtest + forward book (

httpxfor the swarm) - Agents: Claude (financial-research methodology) · OpenRouter (150-LLM swarm) ·

robinhood-tradingMCP for market data - Dashboard: Next.js · Finnhub live quotes — deployable to Vercel